Challenges to the SEC Climate-Disclosure Rule

The proposed Climate-Related Disclosures for Investors rule from the Securities and Exchange Commission faces considerable opposition, including from Commissioner Peirce. On March 21, 2022 she provided this statement to justify her decision to vote against the proposed rule..

It is noteworthy that the arguments for not finalizing the rule are mostly procedural. These arguments do not challenge the fact that the climate is changing, that the consequences of those changes are already very serious, that the proposed rule can help address some of these climate challenges, and that it can help investors make better-informed decisions.

Areas of Contention

Some of the areas of contention include the following:

The SEC’s regulatory authority;

Scenario Analysis;

Materiality;

Scope 3 Problems; and

Difficulties for Small Companies.

Regulatory Authority

The following is from Commissioner Peirce’s comments.

Current SEC disclosure mandates are intended to provide investors with an accurate picture of the company’s present and prospective performance through managers’ own eyes. How are they thinking about the company? What opportunities and risks do the board and managers see? What are the material determinants of the company’s financial value? The proposal, by contrast, tells corporate managers how regulators, doing the bidding of an array of non-investor stakeholders, expect them to run their companies.

The SEC’s mandate is to ensure that investors are provided with accurate, timely and comparable financial information. The Commissioner argues that the SEC is telling companies what actions they should take in response to the climate crisis.

A close reading of the proposed rule (all 490 pages of it) and of the supporting documentation from the TCFD (Task Force on Climate-Related Financial Disclosures) and Greenhouse Gas Protocol (many more hundreds of pages) does not really back up this contention. The focus of the rule is on the provision of climate-related information. The assumption is that investors will then pressure companies to take action based on that information.

Scenario Analysis

Commissioner Peirce continues,

It < the proposed rule > identifies a set of risks and opportunities—some perhaps real, others clearly theoretical—that managers should be considering and even suggests specific ways to mitigate those risks.

The proposed rule and the TCFD standards do, in fact, call on companies to conduct scenario analyses, i.e., they are asked to visualize a range of “what might be” situations, most of which will never happen. Such actions go beyond simply providing information to do with the company’s current financial status. However, it is normal for a company to report on its future prospects. When it comes to climate change there are so many uncertainties that some form of scenario analysis seems to be unavoidable.

We have written a series of posts to do with Scenario Analysis, starting here.

The SEC’s Authority

Many commenters claimed that the SEC did not have the authority to promulgate such a sweeping rule without specific legislation from Congress authorizing it to do so.

Materiality

The concept of materiality crops up a lot in the comments to do with the proposed rule. There are two aspects to this topic. The first is that any significant climate-related risk would already have to be reported in current financial disclosure statements. Quoting Commissioner Peirce once more,

A credible rationale for such a prescriptive framework when our existing disclosure requirements already capture material risks relating to climate change . . .

. . . under existing rules, companies already are disclosing matters such as the risk of wildfires to property, the risk of rising sea levels, the risk of rising temperatures, and the risk of climate-change legislation or regulation, when those risks are material the company’s financial situation.

The other concern to do with materiality is that companies may be required to report climate-related information that is not significant with regard to their overall financial performance.

Scope 3 Problems

The SEC decided to follow the concept of ‘Scopes’, as structured by the Greenhouse Gas Protocol. Scopes 1 and 2 are straightforward and make sense. The same cannot be said about Scope 3 requirements. Further discussion on this contentious topic will be provided in future posts.

Onerous for Small Companies

The proposed rule applies only to publicly traded companies in the United States. Most of these companies are large, and have the resources to address the rule’s requirements. However, these same companies will be calling on much smaller organizations, many of which are not publicly traded, to provide detailed climate-related information. Many of these smaller companies will not be able to provide the required information.

Need for Action

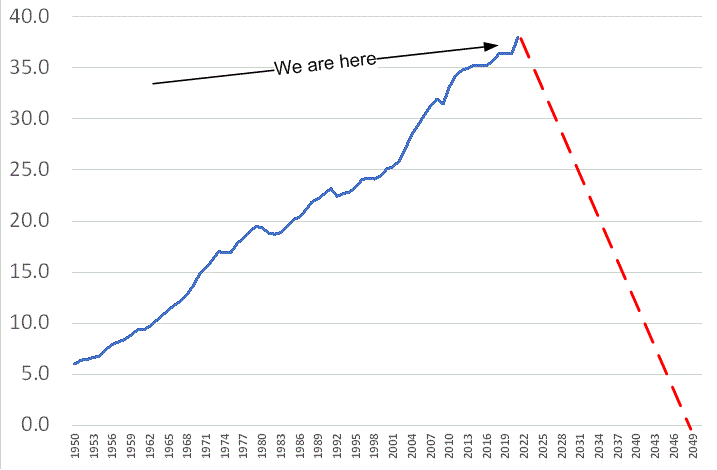

All of the above objections to the proposed rule are fundamentally procedural. They are not to do with the realities of climate change — realities that are becoming increasingly evident just from newspaper and internet headlines.

The chart shows how carbon dioxide (CO2) emissions continue to climb inexorably. The climate challenge is real and urgent. It would be irresponsible to spend months and years arguing over procedural matters at a time when wild fires, floods and drought are threatening the lives of millions of people.

It is not enough just to object. Those who object to the proposed rule need to come up with their own answers.

Information is the starting point. The proposed rule provides a mechanism for finding, organizing and reporting the necessary information.