ESG, Social Justice and the SEC Climate-disclosure Rule

COP27 is drawing to a close. One of the themes of the conference has been to do with financial compensation for those countries which did little to cause the climate problem, but which are disproportionately suffering the consequences. In other words, the response to climate change has morphed from simply controlling rising temperatures to one of social justice. This is a concern.

At this site we are following two proposed regulations from the United States government. The first is the ‘The Enhancement and Standardization of Climate-Related Disclosures for Investors’ from the Securities and Exchange Commission (SEC). If it is authorized, this rule will require public companies to report on their greenhouse gas emissions, and to assess the risks that they face from climate change.

The second proposed regulation that we are following is the proposed update to the ‘Process safety management of highly hazardous chemicals’ from the Occupational Safety and Health Administration (OSHA).

Although the goals and backgrounds to these two documents are very different, they do have the same general intent: to implement management systems and technology to reduce industry’s impact on the health and safety of workers and the people in the community.

One of the most noticeable differences between the two documents is to do with their length. The proposed SEC rule is 490 pages long, and is supported by consensus standards from organizations such as the TCFD. When these standards are included, the proposed rule stretches for nearly 1,000 pages. OSHA’s process safety rule, on the other hand, is just 20 pages long. Moreover, it does not reference many other documents — it is mostly self-contained.

So why are the standards of such different length?

There are, of course, many answers to this question, including,

The SEC rule covers virtually all public companies in the United States, whereas the process safety standard is directed to a much narrower base.

The principles of process safety management were well established before OSHA published its rule in the year 1992. The principles of how to address climate change are, on the other hand, still under development. The proposed SEC rule contains many references and citations that explain why they are saying what they are saying.

The SEC rule will require companies to make massive new investments, whereas the OSHA rule was, for many companies, mostly an extension to what they were doing anyway.

There is, however, another factor that may contribute to the length of the SEC’s proposed rule: ESG or Environmental, Social, and Governance. This is a topic that is not a part of the OSHA standard.

ESG

Traditionally, a company’s primary responsibility is to maximize profits, and to provide a good return to stock holders and others who invest in that company. Other issues, such as ensuring the safety and health of workers or protecting the health of the public and members of the public, are taken care of through the use of regulations and industry standards, and social pressure (including pressure from the investment community).

Increasingly, however, companies are following an ESG philosophy. These companies are called on to address the needs and concerns of a wide range of ‘stakeholders’, including employees, customers, suppliers, communities and even the population of the world at large.

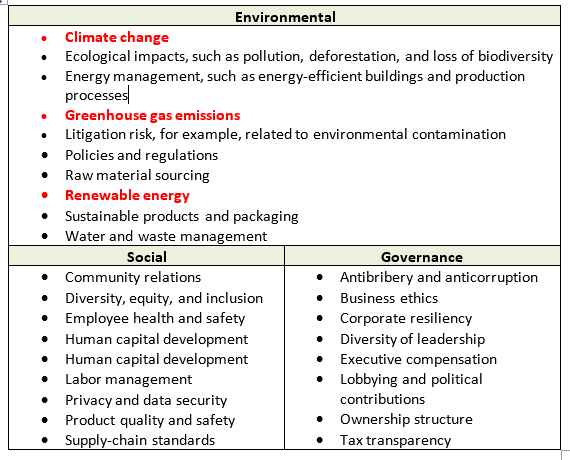

The following Table, which is derived from an FASB (Financial Accounting Standards Board, 2021) publication, shows some of the topics that are included in ESG programs.

In addition to considering the needs of all these stakeholders companies need to consider a wide range of socio-economic issues, including employment practices, diversity, social and cultural ethics, data security and sustainability. In this way of thinking the proposed climate-disclosure rule is perceived as being just one piece of an overall ESG program.

The fact that there are so many “customers” can lead to a lack of focus. In the words of the proverb, a company is likely to be, “Jack of all trades, and master of none.” Indeed, it is likely that the different stakeholders will have different demands. For example, artificial fertilizers are made from natural gas. If a chemical company decides to stop making fertilizers in order to satisfy the climate stakeholders then the price of fertilizers will rise. Hence, its farming customers — who are also stakeholders — will be unhappy.

The SEC Proposed Rule

The SEC’s proposed rule does not explicitly require companies to develop an ESG program. Nevertheless, the document does include 99 references to the term. ESG is implicitly an integral part of the rule.

Lack of Focus

Many business leaders argue that their primary responsibility is to generate a profit for the company’s stock holders. Other social issues can be handled through appropriate legislation. After all, if a company is not profitable then that company will go out of business, taking its ESG activities with it.

Greenwashing

In its proposed rule the SEC expresses a concern to do with ‘Greenwashing’. This concern is bound to crop up when a company has so many different targets to shoot for.

To date, companies have been able to make general statements as to their success in meeting ESG goals. These statements are often difficult to verify. If, however, they are obliged to meet the requirements of the SEC rule then one aspect of the ESG commitment — greenhouse gas emissions — can be measured quantitatively. Moreover, companies will have to report their results in legally-required documents.

Business Leadership

A theme of these posts is that the above differentiation between profitability and social responsibility is not meaningful when it comes to climate change. It makes business sense to adapt to a world where the climate is changing so quickly. In this context, rules and standards from organizations such as the SEC can help a business achieve its financial goals, and also address general concerns to do with climate change. There is no discrepancy between the two goals.